The Market Is Done Debating Risk. Now It’s Testing Execution.

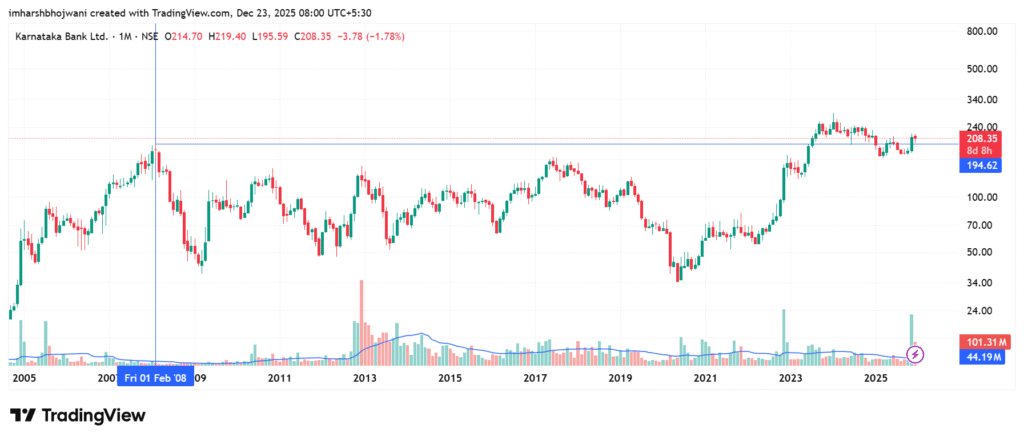

This Karnataka Bank earnings call analysis is not about understanding banking jargon. The terminology is incidental. What matters is what the conversation reveals about where Karnataka Bank stands today and how the market has quietly shifted its expectations.

The market is no longer asking whether Karnataka Bank is safe. That question has already been answered. What investors are now probing, carefully but persistently, is whether the bank can move fast enough now that stability is no longer in doubt.

That shift, from risk to execution, is the real story embedded in this earnings call.

The Signal Was in the Questions, Not the Numbers

Earnings calls rarely reveal truth through prepared remarks. They reveal it through the questions investors choose to ask.

In this call, there was no anxiety around solvency, no suspicion of hidden bad loans, and no defensive posture around capital adequacy. Instead, the questions were operational, specific, and repetitive. They circled around speed, throughput, and organisational friction.

That tells us something important. Karnataka Bank has exited the fear phase. The market has mentally closed the survival file and opened a far less forgiving one: execution.

This is the phase where many bank turnarounds lose momentum, not because numbers deteriorate, but because progress fails to accelerate.

CD Ratio: Not a Definition, a Constraint

The repeated focus on CD ratio sits at the centre of this Karnataka Bank earnings call analysis.

CD ratio measures how much of a bank’s deposits are lent out. A ratio in the low 70s(in case of Karnatka Bank) means a meaningful portion of money is sitting idle, earning low returns instead of generating loan income.

What matters here is not the definition, but the implication. Karnataka Bank does not have a funding problem. It does not have a capital problem. It has a deployment problem.

That is why management keeps returning to CD ratio. Improving it does not require more capital or higher risk-taking. It requires faster loan approvals, better delegation, and fewer internal choke points.

If CD ratio does not move, most other improvements remain cosmetic.

RAM Lending: A Safety Choice, Not a Growth Claim

RAM lending — Retail, Agri, and MSME loans — refers to smaller, diversified loans rather than large corporate exposures.

In this Karnataka Bank earnings call analysis, RAM is not positioned as an aggressive growth lever. It is positioned as a control mechanism.

After a painful corporate credit cycle, RAM reduces the probability that a single mistake can damage the entire balance sheet. That stability is valuable. But it comes with an unavoidable trade-off: speed.

RAM can stabilise earnings and smooth credit costs. It does not, by itself, force a re-rating.

Growth will not come from choosing RAM. It will come from how efficiently the bank executes within RAM.

🔍 Investor Lens: What Actually Matters From Here

This earnings call makes one thing clear: risk is no longer the debate. From here, the market will not reward explanations, intentions, or strategic comfort. It will only reward observable execution.

First, trajectory over targets. Markets do not need CD ratio at 80% tomorrow. They need to see it rise quarter after quarter without drama. A slow, boring climb is more valuable than ambitious targets repeated every call.

Second, silence replacing defence. As long as management is explaining approval processes, delegation structures, or RAM strategy, execution is still in question. Confidence arrives when these topics stop needing explanation because they have stopped being issues.

Third, time as the hidden risk. At this stage, Karnataka Bank’s biggest risk is not asset quality or capital adequacy. It is time. Stable banks that fail to build momentum often remain optically cheap not because markets are blind, but because patience quietly expires.

Investor takeaway:

From here, Karnataka Bank will be judged not by what it avoids, but by how consistently it converts discipline into throughput, without having to explain itself every quarter.

Asset Quality: When the Absence of Panic Is the Signal

Slippages and NPAs were discussed, but without urgency.

(An NPA is a loan that has stopped paying; slippage refers to new loans turning bad.)

The calm tone matters more than the numbers.

If the market believed there was unresolved credit stress, the questions would have been sharper and more adversarial. Instead, asset quality was treated as something to monitor, not fear.

That tells us the survival chapter is closed. What remains is how effectively the bank uses a clean slate.

Recoveries and Write-Offs: A Tailwind That Is Fading

Recoveries from technically written-off loans were also discussed.

(A write-off means the loss has already been accepted in the books; any recovery later flows directly to profit.)

This matters, but only up to a point.

Recoveries helped normalise profits during the cleanup phase. They still add incremental income, but they cannot power a durable growth story. The earnings call implicitly acknowledges that the cleanup dividend is largely behind the bank.

Future performance must come from live lending efficiency, not legacy resolution.

The Phase Karnataka Bank Has Entered — and Why It Is Unforgiving

Banks typically pass through three unspoken phases: survival, cleanup, and execution.

This Karnataka Bank earnings call analysis places the bank firmly in the execution phase. That phase is unforgiving because intent is no longer rewarded. Direction is assumed. Only delivery counts.

This is also where investor patience erodes fastest, because downside risk has already been removed from the story.

Execution phases kill more turnarounds than bad loans ever did.

Leadership Stability and TAT: Throughput, Not Governance Drama

Questions around leadership churn and TAT — turnaround time, or how quickly loans are approved — were not governance scares. They were throughput concerns.

You cannot raise CD ratio if approvals are slow. You cannot speed up approvals without stable authority and clear delegation. That is why these issues surfaced now, and not earlier.

Investors are no longer questioning what the bank wants to do. They are questioning how fast it can do it.

What This Karnataka Bank Earnings Call Analysis Ultimately Tells Us

This Karnataka Bank earnings call analysis does not describe a fragile bank.

It describes a bank that has run out of narrative cover.

The cleanup credit has been earned.

The stability credit is priced in.

What remains is the hardest test in banking: turning discipline into momentum without repeating past mistakes.

If Karnataka Bank succeeds from here, it will be because execution finally matched intent. If it disappoints, it will not be because of NPAs or capital adequacy.

It will be because speed never arrived.

That is the real message embedded in this earnings call, and the only one that matters now.

Frequently Asked Questions

What is this Karnataka Bank earnings call analysis mainly about?

This Karnataka Bank earnings call analysis explains how investor focus has shifted from asset quality and survival to execution speed, lending throughput, and operational delivery after balance-sheet stabilisation.

Is Karnataka Bank still facing asset quality risk?

Based on the earnings call discussion, asset quality risk is no longer the primary concern. Slippages and NPAs were addressed calmly, indicating that major credit stress is largely behind the bank.

Why is CD ratio discussed so frequently in the earnings call?

CD ratio measures how much of a bank’s deposits are converted into loans. In this earnings call, it matters because a lower CD ratio indicates under-deployment of capital, pointing to execution and approval-speed constraints rather than funding issues.

What does RAM lending mean in Karnataka Bank’s context?

RAM lending refers to Retail, Agri, and MSME loans. In this Karnataka Bank earnings call analysis, RAM is positioned as a risk-control and stability strategy, not as an aggressive growth driver.

Do recoveries and write-offs still drive Karnataka Bank’s profits?

Recoveries from written-off loans still add incremental profit, but their impact is reducing. The earnings call suggests that cleanup-driven earnings support is largely over, and future performance must come from live lending.

Is this Karnataka Bank earnings call analysis a buy or sell recommendation?

No. This article is an interpretive analysis, not an investment recommendation. It focuses on understanding business signals, not predicting stock prices.

If you want to read the full transcript, you can access it here as part of this Karnataka Bank earnings call analysis.

Harsh is the creator of Dalal Street Lens, where he writes about investing, market behaviour, and financial psychology in a clear and easy way. He shares insights based on personal experiences, observations, and years of learning how real investors think and make decisions.

Harsh focuses on simplifying complex financial ideas so readers can build better judgment without hype or predictions.

You can reach him at imharshbhojwani@gmail.com

More from Dalal Street Lens

Most Investors Misread Accent Microcell. This Is the Real Business.

Most Investors Misread Accent Microcell. This Is the Real Business. Costco Business Model Explained: Why Costco Feels Different the Moment You Walk In

Costco Business Model Explained: Why Costco Feels Different the Moment You Walk In McDonald’s Business Model Explained: Why It’s Not Really About Burgers

McDonald’s Business Model Explained: Why It’s Not Really About Burgers Jesse Livermore Lessons

Jesse Livermore Lessons How Nassim Taleb’s Trading Philosophy Changed the Way I Look at Confidence in Markets

How Nassim Taleb’s Trading Philosophy Changed the Way I Look at Confidence in Markets Retail Investors vs Institutional Investors

Retail Investors vs Institutional Investors Second Order Thinking in Investing: Four Decisions I Had to Learn the Hard Way

Second Order Thinking in Investing: Four Decisions I Had to Learn the Hard Way Cost Structure Is Destiny

Cost Structure Is Destiny The Attention Economy Trade: Who Really Makes Money When Global Stars Visit India

The Attention Economy Trade: Who Really Makes Money When Global Stars Visit India India’s Data Centre Supercycle: The Simplest Explanation of Colo, Cloud and AI Infrastructure

India’s Data Centre Supercycle: The Simplest Explanation of Colo, Cloud and AI Infrastructure