Why the most misunderstood policy move in the world deserves quieter thinking

The Day Everyone Cheers

The day the Federal Reserve cuts interest rates, the mood is almost predictable.

Markets bounce.

Headlines turn optimistic.

Experts say the word liquidity like it will cure everything.

It feels like relief.

But every time I see a rate cut being celebrated, I feel the same quiet discomfort, the kind you feel when a doctor smiles a little too politely before prescribing medicine.

Because here’s the uncomfortable truth we rarely sit with:

Strong economies don’t need rescue. Weak ones do.

And rate cuts are not rewards.

They are responses.

What a Rate Cut Actually Is

At its simplest, a rate cut means this:

The US central bank lowers the interest rate at which money flows through the financial system, hoping that:

- Borrowing becomes cheaper

- Spending increases

- Investment resumes

- Growth stabilizes

What the Fed can do:

- Influence borrowing costs

- Affect liquidity conditions

- Shape financial sentiment

What it cannot do:

- Force businesses to invest

- Create consumer confidence

- Prevent structural slowdowns

This distinction matters more than most coverage admits.

The Medicine Analogy

Think of rate cuts as medicine.

You don’t take medicine when you’re thriving.

You take it when:

- Something feels off

- Symptoms aren’t visible yet

- But tests suggest trouble ahead

Historically, the Fed cuts rates when:

- Growth momentum slows

- Credit markets tighten

- Financial stress begins to surface beneath the surface

That’s not celebration territory.

That’s precaution.

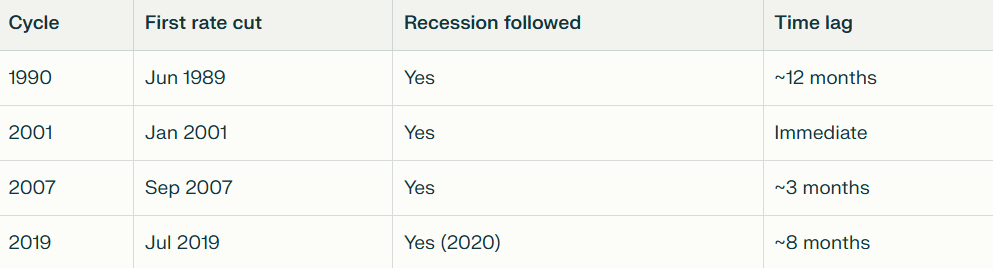

What History Quietly Shows (Data, Not Opinion)

Let’s ground this in evidence.

Sources:

Federal Reserve (FRED), NBER recession dates

This does not mean:

- “Rate cuts cause recessions”

It means:

Rate cuts usually arrive because the risk of recession is already rising.

Correlation doesn’t imply causation, but ignoring correlation is intellectual laziness.

Why Markets Still Celebrate

So why do markets cheer?

Three reasons:

1. Valuation Math

Lower rates increase the present value of future cash flows, especially for long-duration assets like growth stocks.

2. Liquidity Illusion

Cheaper money feels like easy money, even when lending standards are tightening.

3. Relief Bias

Humans confuse relief with recovery.

Painkillers reduce pain.

They don’t heal fractures.

The Quiet Redistribution Nobody Talks About

Rate cuts don’t help everyone equally.

They benefit:

- Borrowers

- Highly leveraged companies

- Asset holders (temporarily)

They hurt:

- Savers

- Pension funds

- Insurance companies

- Retirees dependent on interest income

This redistribution is real, measurable, and rarely discussed, even though it affects long-term economic stability.

According to BIS and IMF research, prolonged low-rate environments:

- Compress bank margins

- Encourage risk-taking

- Distort capital allocation

These are not side effects.

They are trade-offs.

Why Markets Sometimes Fall After Rate Cuts

This confuses many.

“Rates are down, why is the market nervous?”

Because experienced investors don’t ask:

What did the Fed do?

They ask:

Why did the Fed feel forced to do it?

The first rate cut is often the most dangerous one, not because it’s harmful, but because it confirms weakness.

Later cuts matter more.

Early cuts reveal more.

Cheap Money Is Not Easy Money

Lower rates don’t guarantee:

- More lending

- More investment

- More growth

During early rate cut cycles:

- Banks often tighten credit standards

- Businesses delay expansion

- Consumers remain cautious

This is why economists track:

- Credit spreads

- Lending surveys

- Bond-market stress

Not just policy rates.

A Simple Framework to Read Any Rate Cut

Use this five-question lens every time:

- Why now?

What changed recently? - What stress is visible?

Jobs, growth, inflation, credit? - What stress is invisible?

Funding markets, leverage, confidence? - Who benefits immediately?

Borrowers or asset holders? - Who pays quietly?

Savers, institutions, long-term stability?

This framework works across cycles, countries, and headlines.

What This Means for an Average Person

- Loans: May get cheaper, but jobs matter more

- Fixed deposits: Returns usually fall

- Investments: Volatility often rises before clarity arrives

- Expectations: Should be tempered, not excited

Rate cuts buy time.

They don’t buy certainty.

What This Article Is NOT Saying

To be clear:

- Rate cuts are not “bad”

- Markets don’t have to fall

- Growth can recover

This is not fear.

This is interpretation.

Understanding signals doesn’t make you pessimistic.

It makes you prepared.

FAQs

Are rate cuts bad for the economy?

No. They are supportive tools — but usually deployed when growth is under pressure.

Do rate cuts always lead to recessions?

No. But historically, the first cut often signals rising risk.

Why do stocks rise after rate cuts?

Short-term liquidity and valuation effects — not immediate economic healing.

How long do rate cuts take to work?

Anywhere from 6 to 18 months, depending on confidence and credit conditions.

The most dangerous misunderstanding in markets is confusing action with assurance.

Rate cuts are action.

They are not reassurance.

They tell a quiet story — one that rewards those who listen carefully instead of cheering loudly.

Rate cuts are a sign of concern, not celebration.

And understanding that difference is not pessimism.

It’s maturity.

If you liked this blog, you might enjoy my previous ones as well:

👉 Why Cheap Stocks Trap You — The Psychology Behind It

👉Why Nifty Is at All Time Highs but Your Portfolio Is in the Basement

👉AI Won’t Crash Like 2000. It Might Correct Like 2008 — When Reality Finally Shows Up.

👉Strong USD Is Not a Modi Issue or a Congress Issue — It’s Global

👉 Why We Feel Smarter After a Stock Falls: The Psychology of Market Regret

👉 Why Comparing Your Portfolio to Others Destroys Your Returns

👉Is Your Stock a Hidden Pump-and-Dump?

Harsh is the creator of Dalal Street Lens, where he writes about investing, market behaviour, and financial psychology in a clear and easy way. He shares insights based on personal experiences, observations, and years of learning how real investors think and make decisions.

Harsh focuses on simplifying complex financial ideas so readers can build better judgment without hype or predictions.

You can reach him at imharshbhojwani@gmail.com

More from Dalal Street Lens

Most Investors Misread Accent Microcell. This Is the Real Business.

Most Investors Misread Accent Microcell. This Is the Real Business. Costco Business Model Explained: Why Costco Feels Different the Moment You Walk In

Costco Business Model Explained: Why Costco Feels Different the Moment You Walk In McDonald’s Business Model Explained: Why It’s Not Really About Burgers

McDonald’s Business Model Explained: Why It’s Not Really About Burgers Jesse Livermore Lessons

Jesse Livermore Lessons Karnataka Bank Earnings Call Analysis – November 2025

Karnataka Bank Earnings Call Analysis – November 2025 How Nassim Taleb’s Trading Philosophy Changed the Way I Look at Confidence in Markets

How Nassim Taleb’s Trading Philosophy Changed the Way I Look at Confidence in Markets Retail Investors vs Institutional Investors

Retail Investors vs Institutional Investors Second Order Thinking in Investing: Four Decisions I Had to Learn the Hard Way

Second Order Thinking in Investing: Four Decisions I Had to Learn the Hard Way Cost Structure Is Destiny

Cost Structure Is Destiny The Attention Economy Trade: Who Really Makes Money When Global Stars Visit India

The Attention Economy Trade: Who Really Makes Money When Global Stars Visit India